Market Commentary

We have been positive on the markets over the 2nd half of 2025 despite seemingly narrow participation and we believe the positive trajectory continues for 2026 given rates are on a downward slope, there is continued support from government/fiscal side, companies are able to manage costs well, and AI is driving a meaningful increase in productivity.

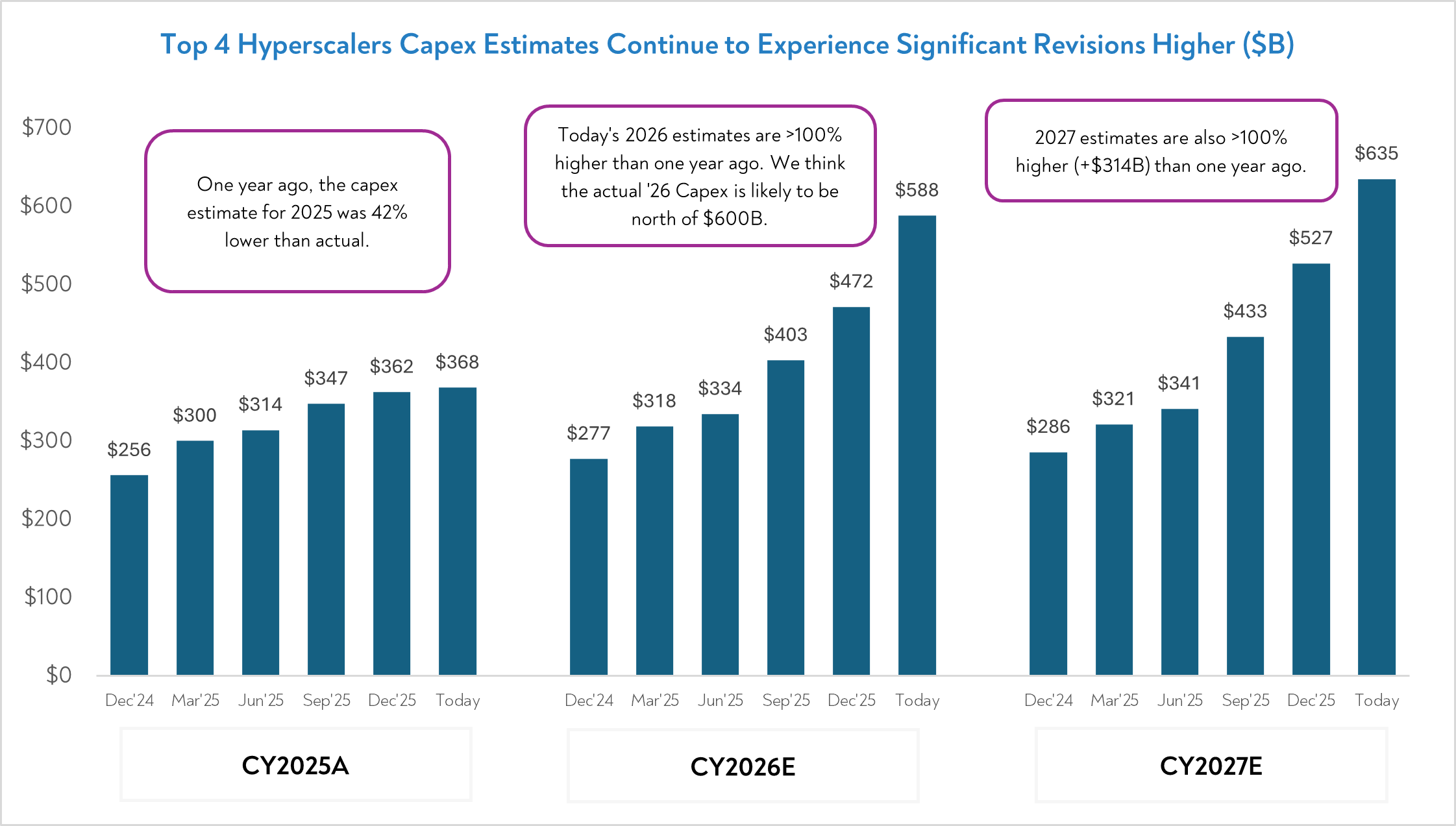

For any type of investor across all asset classes, impact of AI has to be top of mind because either directly or indirectly, AI has been one of the main drivers of the growth of the US economy for last couple years. The magnitude of AI related capex investments especially driven by large cap companies has been phenomenal and has contributed significantly to the bounce back in the indices since April lows of 2025. Given our positive bias on AI investments, and accelerating AI adoption, we think this helps continue the current market trends.

Our current portfolio is balanced with our barbell approach (M&A/active engagement on one end, with AI/positive rate of change on the other). We have continued to deprioritize ‘low valuation’ as a criteria for our company selection and increasing the ‘positive rate of change’ (in revenue growth and profits), as a higher prioritization metric.

Current Assessment of Macro and Review of 2025

President Trump’s election at the end of 2024 created expectations of rates going down substantially, reduction in regulations, and a broad restart of a sluggish economy weighed down by post-COVID digestion plus high interest rates. This narrative helped 2025 start with a strong promise of a reacceleration in base economy, however, that promise didn’t come to fruition in 1H’25 and the announcements of tariffs threw a further wrench in economic growth. Capital flowed to the only area of the economy that was showing strong promise and growth – AI.

Hence, in 2025 we saw the continuation of theme that AI investments pretty much holding the economy despite anemic growth elsewhere. The summer of 2025 was all about AI re-acceleration, strengthened by explosive adoption of tokens and AI agents especially in the 3-Cs (Coding, Customer Service and Content).

The rapid rise in AI adoption also created an additional narrative that all software is going to get disrupted/subsumed by AI. This led to a dramatic reduction in the multiples of most software companies. It took us a couple months to figure out why software multiples kept compressing and whether it was a tactical buying opportunity vs a long-term seismic shift. Despite many software companies reporting good numbers and low valuations, the stocks kept going down in software. This trend has further accelerated in 2026. Our diligence last year led us to believe that there is much more going on underneath the surface which led us to take a more balanced view on software despite very attractive valuations. There are big seismic shifts in the world of technology and value is migrating across the broader technology stack, all of which we are paying attention to and those we have covered in detail in our prior letters.

Our investing takeaway has been that rate-of-change has become an even stronger requirement for stocks to work (as opposed to valuation). Since inception, Scalar Gauge always had two pillars to our investment process – rate of change (in fundamentals) and potential buyout by a strategic/PE. In late 2025, we realized that majority software companies that had valuation support to be acquired by PE no longer had the positive rate-of-change due to budgets flowing towards AI, and in fact, multiples kept compressing due to uncertainty posed by AI risk in the mid-long term.

We re-prioritized to ensured we stay on the right side of the AI juggernaut that is impacting not just the technology industry but pretty much the entire economy, and because we think AI is still in the early stages, the tables have not been set. Infact, we could still be in the early stages. In the past, we have owned and written about several semiconductor, networking and other technology companies, and based on our diligence, we are finding substantial positive rate of inflection in many technology segments and companies.

With respect to our portfolio composition, currently we are maintaining a barbell approach – we are involved in just a couple software companies that are trading very attractively for a buyout with positive change in fundamentals along with it. On the other hand, we have invested in high quality technology companies that are showing durable inflection in their business and valuation partially due to AI, but also due to other architectural shifts in the tech stack. We measure rate-of-change on several operating metrics and KPIs, but at the end it all has to show up clearly in accelerating financials – in the form of revenue growth or margins. We do believe this barbell approach gives the best risk-reward profile for the next 1-2 years.

Finally, on the broader economy, more of the same will likely continue because we are not seeing fundamental inflection either through top-down macro drivers or through our bottom-up company research. We don’t see any near-term turning point for the non-AI economy as rates are not going down drastically (although the trend is to the down and hence positive from a demand standpoint). Housing, industrial, automotive, consumer etc. are all waiting for economy to improve with lower rates and the benefits of AI to flow through the main street. AI investments must stay strong until that transition can happen successfully in order to avoid any air-pocket. The conditions are positive, however, we still need to see proof points to assess a broader economy acceleration. For now, Technology and AI continue to be the focal point of any meaningful rate of change and that’s where we are spending majority of our time and energy.

The AI Investment Cycle Should Have a Long Duration

We view the AI capex cycle as still in early stages and durable. The bulk of observable AI demand has been driven by consumer-facing use cases such as search, content generation, and productivity copilots, which require comparatively modest levels of integration and change management. Enterprise adoption, despite growing fast, still remains in the early innings. Many large organizations continue to be in pilot mode, working through data governance, security, workflow redesign and ROI validation before scaling up deployments. As enterprises figure out these, enterprise workloads should drive a materially larger and more persistent wave of infrastructure investment.

Later this year, the market will likely begin to focus on 2027 spending expectations. The pace of 2027 investments will be dictated by the use cases and success stories of 2026. Currently, we believe these investments are likely to continue, but we remain very data-driven (especially over the next several months) to assess whether there is a meaningful slowdown or acceleration for 2027.

AI spending is set to continue, driven by the largest and most systemically important companies. These firms have the most to lose from falling behind, the largest cash balances to deploy, and large shareholder bases that reward long-term strategic dominance. Their equities are broadly owned, their platforms are foundational and underinvestment carries existential risk. In this context, sustained spending is not discretionary; it is defensive.

We also believe that AI Return on investment is no longer theoretical. When companies valued in the trillions explicitly state that AI investments are generating acceptable or attractive returns and commit to continued capital deployment, that signal carries weight. These are the most informed buyers in the market, operating with full visibility into costs, productivity gains and competitive positioning. The debate over whether the ROI exists is increasingly irrelevant; it is being resolved by those writing the largest checks. Moreover, the value created by incremental intelligence is compounding at a rate that outpaces the growth in underlying costs.

The industry has already passed the critical inflection point. What began as a “zero to one” phase of experimentation has transitioned into large-scale deployment and optimization. The core infrastructure decisions have been made, and capital has been committed. The focus is now on scaling and extracting increasing returns from an installed base, rather than questioning the validity of the technology itself.

This shift reframes the capex versus opex discussion. AI infrastructure is inherently front-loaded. Capital expenditures are incurred upfront, while the economic benefits accrue over time as models improve and utilization increases. Hence, the effective cost per unit of intelligence declines with scale. Rather than curtailing spend, this dynamic in fact incentivizes further investment, as each incremental dollar of capex supports a disproportionately larger increase in productive output.

At the core of this cycle is the exponential nature of compute, network, storage, semiconductor and hardware demand. Improvements in model capability expand the set of economically viable use cases, which in turn drives additional demand for the supporting infrastructure. This feedback loop reinforces itself. The trajectory is not linear as different companies and different models will lead or lag, however, the implications for infrastructure demand are expected to be with us for the next several years.

AI & The Impact on Software

Much has been written and debated over the last couple months on the disruption of software industry due to arrival of AI agents. At this point, we believe it is widely disseminated and the software valuation multiples do reflect this new AI reality. Near-term, we do think that numbers for software companies don’t get worse because of acute focus by management teams and ability to cut costs. Long-term, there is a case that can be made that as AI exponentially gets better, there is acute pressure on terminal value of any software company. There may be a small number of software companies that can benefit from AI, but a large majority will struggle. We are staying away from 3Cs (Content, Coding and Customer Service) and only looking at a very selective group as described next.

Assessing the Next 25 Years Compared to the Last 25

We thought to incorporate some high-level thoughts given the rapid changes going on in the world of technology. Over the past 25 years, the applications and consumption were largely driven by the infrastructure (internet, mobile) that came before. Capital was plentiful, marginal costs in software were close to zero, and distribution scaled faster than balance sheets. Venture capital naturally concentrated at the application/consumption layer because that is where capital efficiency was highest. New categories could be created with small teams, limited fixed investment, and rapid iteration cycles.

This environment produced hundreds of VC-backed winners across Cloud, SaaS and consumer internet. Competitive advantage was largely transient and what mattered most were UI, branding, sales execution and distribution mattered more than deep operational moats. Moore’s Law and cloud abstraction masked inefficiencies and allowed software businesses to scale without confronting physical constraints. Valuations followed narratives around TAMs, and growth came easy.

Infrastructure (networking, semiconductor, storage, data center), by contrast, was starved of capital during the last 25 years and very limited innovation or competition was funded. Infrastructure businesses were capital-intensive, slower to scale, and poorly suited to venture economics. Funding was limited due to the fact returns were back-weighted, and valuations reflected skepticism and cyclicality rather than strategic. Additionally, many of the manufacturing gains were mostly incremental rather than immensely more complex (which we are currently experiencing today). Physical bottlenecks existed but were not constraining the overall system.

It seems that the world is at another turning point now. Our high level viewpoint is that the next 25 will be defined by scarcity rather than abundance. Compute, power, data center capacity, advanced manufacturing yields, materials, and energy are no longer abstract inputs the world ignores. Progress is increasingly gated by the real world. Marginal costs are rising, fixed costs dominate and failure is expensive. Iteration cycles are constrained by fabrication timelines, supply chains and energy availability rather than code releases (though some new AI-centric startups are proving that they can ship faster than incumbents which is helping to cause a broader dislocation relative to pre-AI era software companies).

As a result, competitive advantage is migrating upstream. Control over scarce inputs now matters more than product differentiation. Scale is no longer just a distribution advantage, it’s required to participate (e.g., balance sheets matter). The nature of capital itself is changing, from generalist and duration-insensitive to concentrated, strategic and long durations.

This shift probably leads to a drastic consolidation in the application layer (mostly SaaS/Cloud/Internet). This last wave/regime supported dozens or hundreds of application-layer competitors (e.g., there are >100 CRM companies today), the next regime may only support a handful of economically superior players in a given segment. Market structures increasingly resemble oligopolies or regulated utilities rather than fragmented competitive fields. As a student of history, we have seen these application and infrastructure waves alternate and dominate over decades. For example, the printing press during 1450-1550, canals and railroads in early 1800, electric grid during 1880-1930, automotive during early 1900, semiconductors in late 1900s and internet during the 2000 era. It would seem to us that the next infrastructure wave is upon us, and the last generation of application age is fading. If AI is as big of a change as any of those prior large scale infrastructure inflections, then it is very unlikely that we are done with AI investments in 2026. We do think AI is a much bigger generational shift that will last a few decades.

Hence, this next era is likely to experience much more vertical integration and stack compression, where innovation moves into infrastructure, manufacturing processes, materials science and systems optimization. These advances are slower, more capital-intensive and much harder to replicate. There will, of course, continue to be some value accrued at the application/consumption layer, we just think that the value creation and capture will look fundamentally different in the future than it has in the past.

If our long-term view is correct, then we are still in the early stages of a monumental shift and a very different world order than how it looked in the recent history. Of course, the rate of change in different segments is already showing us the datapoints and clues on what’s next. We remain observant and open minded to capture the value creation wherever the durable and sustainable rate of change will drive us to.